Can you buy a home when you already own one?

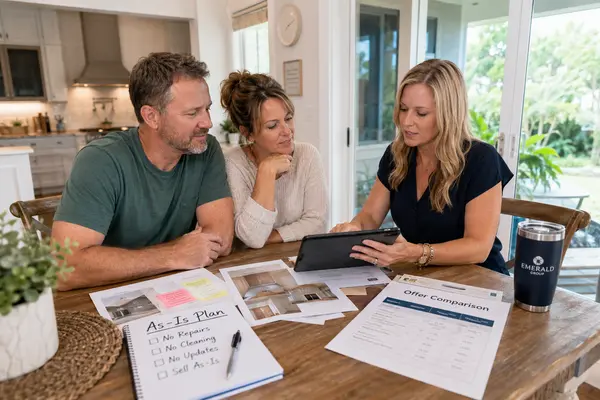

It's Andrew and Kristen with the Emerald Group.

All right, so this week we decided we were going to talk about - do you need to

sell your own home before financing another one?

Because if you're paying cash, it doesn't really matter, right?

We’re going to skip that portion of let's say you're financed in one home

and you're thinking about purchasing another home.

We actually have some customers going through this right now.

We figured there's some good information there.

What if your current home is a VA loan?

Okay, if your current home is a VA home,

you can still purchase another VA home.

You have four hundred eighty four thousand

three hundred fifty dollars of entitlement for your VA eligibility.

You can still go over that and lenders correct me if the numbers change occasionally changes on us.

So, $484,350 and then anything you go above that you're going to have to pay a down payment on so let's say “Home A” is 200,000.

You'll still have two hundred eighty four thousand three hundred fifty dollars to go up to

your next home without having to worry about it down payment.

So VA is definitely possible to do this.

Now let's talk debt to income ratio.

Do you need to actually close and sell the first home before purchasing the next one. Maybe

Let’s elaborate on that.

Basically what the lender is going to look at is your debt to income ratio.

They will count your mortgage on your first home that you're living in

so that mortgage payment plus the new mortgage payment plus any other debt you have

credit cards, car loans, student loans, all that good stuff.

If all of that equals under a certain percentage of your income,

Then you should be good to continue without have to sell and close on your current home.

So that leads us to kick out Clauses in the contract.

Let’s say you're living in a home now and in the given situation that we're talking about now,

they're fixing up the home,

but they found another home that they just fell in love with they weren't even

really looking at just it just happened that's part of it.

That's part of home shopping.

And we decided to secure that property

and the sellers and Agent on the other end put in a kicked out clause to protect their Sellers.

The kick out clause is basically stating -

Hey, we're going to keep showing the

home as the seller and if an offer comes through

and we want to take it will let the buyer know that secured the property already

In this case the Seller’s are going to give them in this case 72 hours which is kind of typical but you can always change the times, right?

Anywhere from 48 to 72 hours is typical and it’s basically stating - Hey selling your home is not a contingency.

Given the following example - our contract what it stated was hey,

we're buying said home but we need to sell this one first. So, we'll put a closing date of let’s say

two months or three months out. They accepted it.

Now, if a better offer came through they do a kick out and they tell us that

we have to remove that contingency that says this home has to sell.

If your debt to income ratio is good than you’re good to continue.

Which luckily for us because it was then they were able to do both

and they didn't lose a deal now if things weren't able to then they

wouldn't be able to remove that contingency.

They would have lost that house and the sellers would have taken another contract,

right? If our debt to income wasn’t good, we would have lost it.

Before you start trying to figure out paying stuff off

We suggest you talk with a local lender first see

where you're at with your debt-to-income because

you might be paying step up that you won't have to pay off.

All in all – it is very possible to purchase a financed home while you still have financing on your home. We will get into the nitty gritty of other situations over the next few weeks

Categories

- All Blogs (156)

- 30A Communities & Condos (10)

- Communities and Condos on the Emerald Coast (24)

- Destin Communities & Condos (8)

- Fort Walton Beach Communities & Condos (9)

- Home Buying Tips (9)

- Home Selling TIps (8)

- Investment & Rental Strategy (9)

- Local Real Estate Answers (60)

- Military Relocation & VA Buyers (13)

- Navarre Communities & Condos (6)

- Niceville Communities & Condos (4)

- Panama City Beach Communities & Condos (1)

- Pensacola Communities & Condos (1)

- Waterfront & Coastal Homes (5)

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "